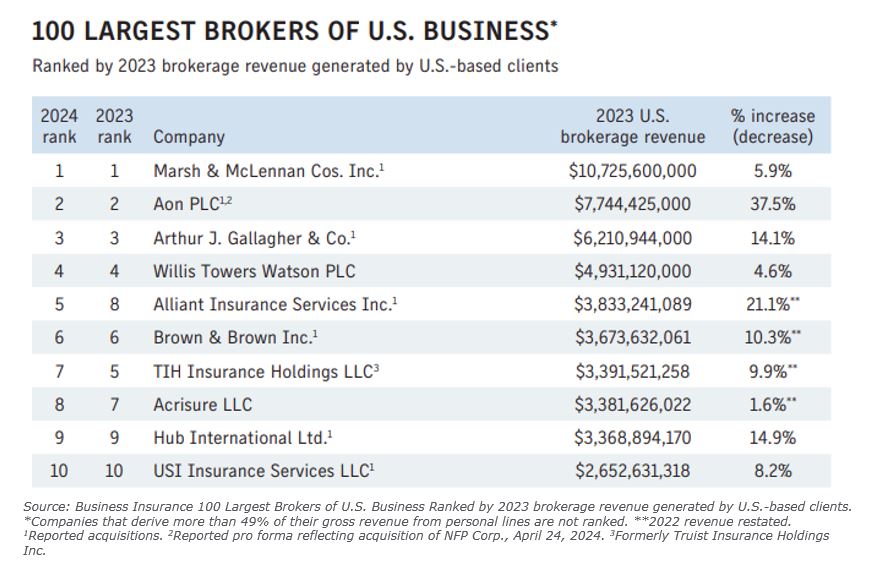

Business Insurance recently published their annual report on the Top 100 Insurance Brokers, ranked by U.S. revenue for 2023. For the fifth year in a row (since 2019), the top 10 firms are exactly the same, with only slight shifting of positions over that span.

This year, the top 10 U.S. brokers’ revenue totaled a resounding $49.9 billion and represents 66% of the total top 100 revenue ($75.5 billion). While the top 100 and top 10 firms grew by 15.0% and 12.8% year-over-year (YoY) respectively – the percentage of revenue for the top 10 has actually trended down over the last few years – due to more growth in the 11-50 firms.

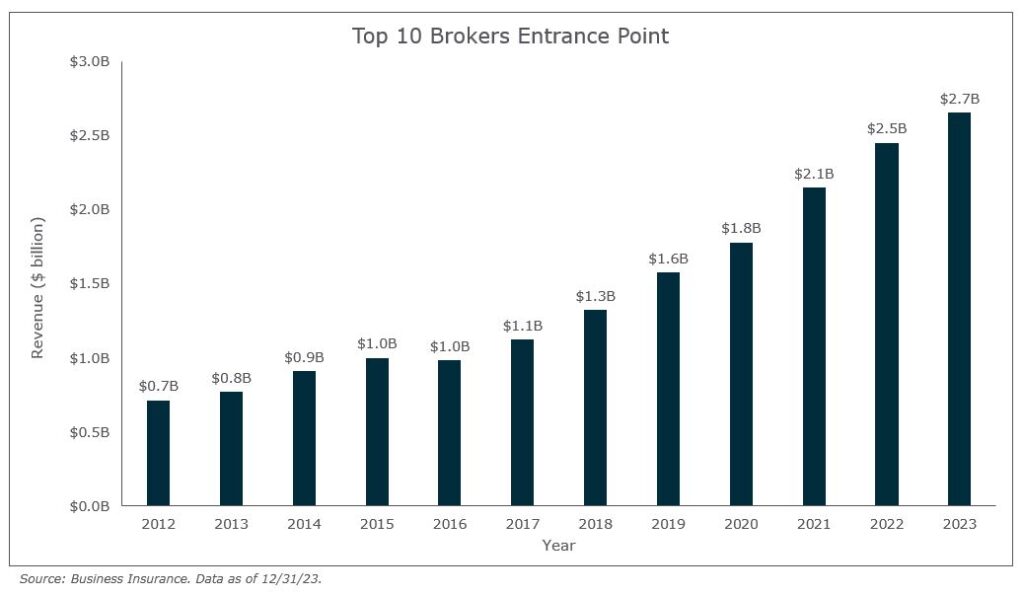

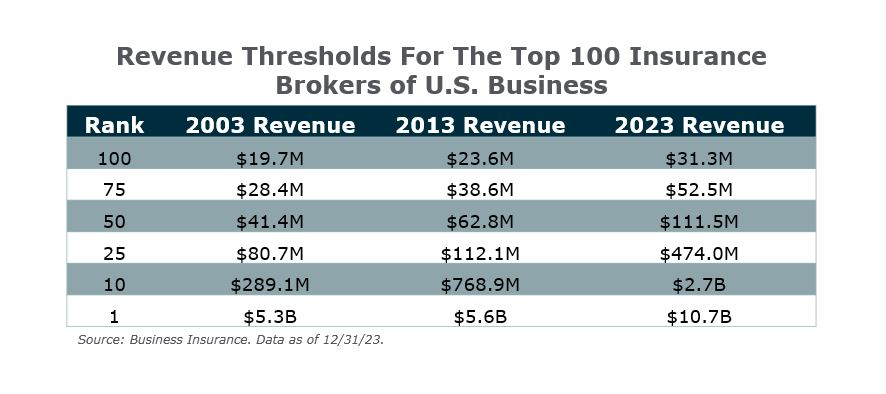

Even so, to enter the top 10 U.S. insurance brokers’ bracket a firm would need a staggering $2.7 billion in revenue. This is compared to just $768.8 million needed 10 years ago in 2013, a 245% increase in this revenue threshold.

Newsworthy takeaways from the top 10 list

The biggest move in the top 10 was made by Alliant Insurance Services who jumped three spots (going from 8 to 5) on $3.8 billion in revenue, an increase of 21.1% YoY. This marks the seventh year in a row that Alliant has delivered double-digit revenue growth since entering the top 10 in 2018. According to CEO Greg Zimmer, “More than two-thirds of Alliant’s revenue growth was organic.” Even so, Alliant announced 16 merger & acquisition (M&A) transactions in the U.S. in 2023.

“Alliant is well positioned in the market in large part because of its long-time focus on specialties, its consistent private-equity support, its attractive employee-equity program and a diversified book of business,” said John Wepler, chairman and CEO of MarshBerry. “They’re flirting with what we call the perfect score, the ‘rule of 50,’ that’s 35% EBITDA (earnings before interest, taxes, depreciation and amortization) margin and 15% organic growth,” said Mr. Wepler. “Extremely strong organic growth and a strong margin is a discipline that very few have.”

In May 2024, Truist Financial Corporation finalized its sale of Truist Insurance Holdings, Inc. to an investor group, led by private equity firms Stone Point Capital and Clayton, Dubilier & Rice. The new entity, now named TIH Insurance Holdings LLC, dropped two spots in the top 10 (from 5 to 7) to $3.4 billion in revenue, with a YoY increase of 9.9%. This ranking drop might be more of a reflection of Alliant Insurance Services’ performance in 2023 and leapfrogging TIH, than anything else.

So, what might this transition mean for TIH’s future growth? “It dramatically improves our positioning,” said TIH’s CEO John Howard. “It means that we have more agility than we had in the past. We’re no longer subject to the risk appetite and regulatory requirements of a bank. We’re able to focus all of our time, energy, and resources on insurance.”

“They’ve become liberated,” said John Wepler. “They have a national platform. They have a portfolio approach with all these distinctive brands. They know how to acquire and integrate. They’ve got a really strong wholesale operation. They’ve got a diversified line of business, from retail and commercial to sophisticated employee benefits with actuarial compliance.”

In December 2023, Aon plc made a big headline splash with the announced acquisition of NFP Corp. in one of the largest insurance broking deals in history. The move by Aon helps them to better compete against Marsh McClennan Agency in the middle market and small commercial segments. NFP was ranked #13 in 2023 (based on 2022 revenue) before being acquired. The result for Aon was a big jump in reported U.S. revenue, growing 37.5% in 2023 to $7.74 billion, with the pro forma reflecting the NFP acquisition. While Aon’s overall reported revenue closes the gap on Marsh & McLennan, Aon still remains the #2 firm in the U.S. (and the world).

Firms in the top 100 that sold in 2023

As previously mentioned, two of the biggest newsworthy deals in 2023 were the Truist Insurance Holdings, Inc. sale to private equity firms Stone Point Capital and Clayton, Dubilier & Rice, and Aon’s acquisition of NFP Corp. While NFP no longer exists on the top 100 list, Truist Insurance Holdings continues to be listed as TIH Insurance Holdings LLC.

Here are the other firms on the top 100 list that sold in 2023:

- The Graham Company was acquired by Marsh McLennan Agency in August 2023. The Graham Company was ranked #63 in 2023 (based on 2022 revenue) before being acquired.

- Fisher Brown Bottrell Insurance Inc. was acquired by Marsh McLennan Agency in April 2023. Fisher Brown Bottrell Insurance was ranked #72 in 2023 (based on 2022 revenue) before being acquired.

- Cadence Insurance Inc. was acquired by Arthur J. Gallagher & Co. in November 2023 from Cadence Bank. Cadence Insurance was the second largest bank-affiliated insurance brokerage in the U.S. and ranked #42 in 2023 (based on 2022 revenue) before being acquired.

- Eastern Insurance Group LLC was acquired by Arthur J. Gallagher & Co. in November 2023 from Natick, Massachusetts-based Eastern Bank. Eastern Insurance was ranked #52 in 2023 (based on 2022 revenue) before being acquired.

Biggest movers in the top 100

As firms are acquired and drop off the list, it is natural for other firms to move up several spots, which is not always an indictment of their own performance. It’s much tougher to move up the list the higher you go, because those larger firms are much more rarely sold and unincorporated (NFP being the exception this year). While strong organic growth continues to be a driver for firms moving up the top 100 list, M&A activity is often the key to significant movement.

In 2023 there were 807 announced M&A transactions, a drop of 11.9% from the previous year. However – high firm valuations, consolidation goals and private capital investments were still strong drivers of M&A activity in 2023. Of the top 100 brokers, 45 of them transacted one or more deals in 2023, representing 67.4% of the U.S. insurance brokerage M&A market.

Here are eight firms (five PE-backed, three independently owned) who have moved up six or more spots on this year’s list, due to M&A activity, organic growth or both.

- Keystone Agency Partners LLC makes another big jump on this year’s list, moving up eight spots to #38 (after moving ten spots last year) with $229.9 million in revenue (a 66.8% YoY increase). This Bain Capital Credit backed firm was helped by the 24 publicly announced deals completed in 2023, after completing 22 deals in 2022.

- Alkeme Inc., backed by GCP Partners, who debuted on the top 100 list in 2021 at #64 – breaks into the top 50, moving up six spots to #49 with $114 million in revenue (a 21.3% YoY increase). Alkeme completed 15 publicly announced transactions in 2023, after completing six in 2022.

- Inszone Insurance Services, backed by BHMS, debuted on the top 100 list last year at #65. This year, Inszone breaks into the top 50, moving up 15 spots to #50, with $111.5 million in revenue (a 61.4% YoY increase). Inszone had an aggressive M&A year completing 45 publicly announced transactions in 2023, after completing 25 in 2022.

- Oakbridge Insurance Agency received an equity investment from Audax Private Equity in September 2023. Oakbridge moved up 13 spots to #56 with $100.1 million in revenue (a 56.4% YoY increase) and completed 14 publicly announced transactions in 2023, and seven in 2022.

- Privately owned Ansay & Associates LLC moved up 10 spots to #77 with $49.9 million in revenue (a 6.0% YoY increase). Ansay & Associates did not publicly announce any M&A transactions in 2023 or 2022.

- King Insurance Partners, backed by BHMS, debuted on the top 100 list last year and continues its growth, moving up 15 spots on this year’s list to #79 with $48.4 million in revenue (a 42.1% YoY increase). King Insurance Partners completed 9 publicly announced transactions in 2023, after completing 16 in 2022.

- Privately owned Swingle, Collins & Associates has moved up nine spots to #88 with $42.6 million in revenue (a 29.9% YoY increase). Swingle, Collins & Associates did not publicly announce any M&A transactions in 2023 or 2022.

- Privately owned Commercial Insurance Associates LLC, who debuted on the top 100 list last year,has moved up eight spots to #91 with $40.4 million in revenue (a 26.9% YoY increase). Commercial Insurance Associates did not publicly announce any M&A transactions in 2023 or 2022.

Takeaways from the top 50 insurance brokers

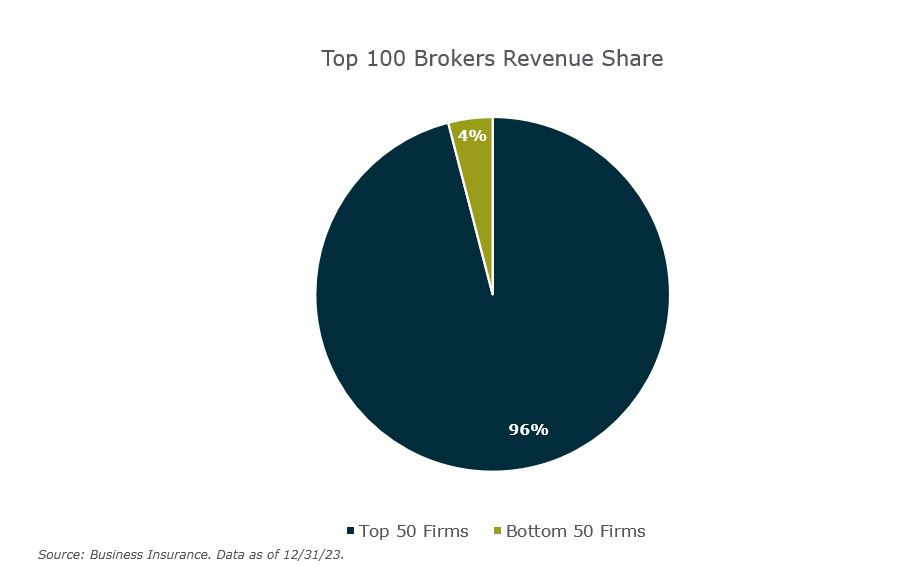

The top 50 firms in 2023 represent $72.5 billion in revenue – which is 96% of the total revenue for the top 100. In 2023 a firm needed over $111.4M to break into the top 50, a 78% increase in this revenue threshold vs. 2013 when firms needed $62.7M to get into the top 50.

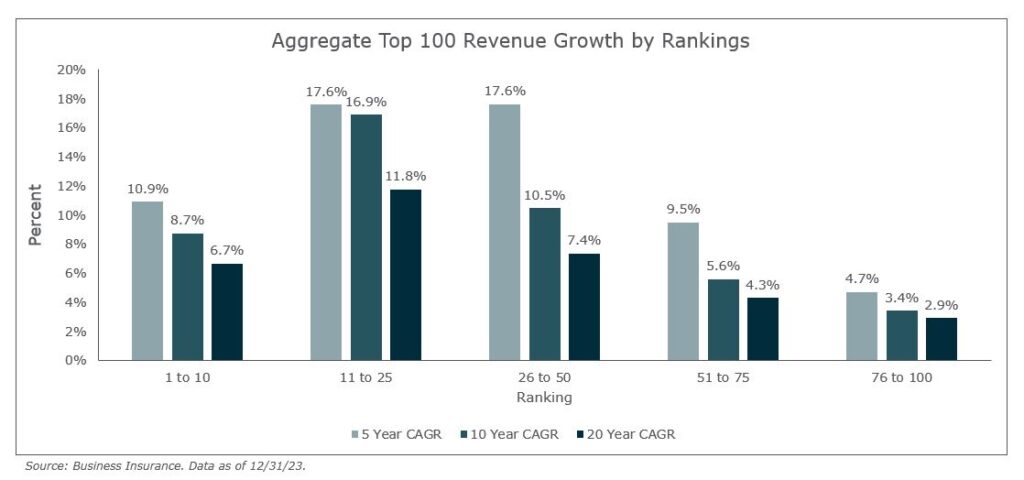

There is a clear growth trend dividing the top 50 (with 96% of the total revenue) and the bottom 50 (with 4% of the total revenue) on the top 100 list – especially for the 11-50 ranked firms. The average compound annual growth rates (CAGR) for the 11-50 firms are significantly higher than the 51-100 ranked firms. The average 5-year CAGR for firms ranked 11-50 is 17.6%. But for firms ranked 51-75, the CAGR drops to 9.5%. And drops even further for firms ranked 76-100 with 4.7% CAGR. This speaks volumes to how quickly and consistently these larger firms are growing, and how challenging it is for smaller firms to be consistent in their growth in order to keep pace.

This challenge for the bottom 50 firms also represents an opportunity for other firms, on the outside, looking in, to break into the top 100 list.

Opportunity to enter the Top 100?

While the overall YoY revenue growth of the combined top 100 firms was 13.5%, it’s interesting to note that 35 of those firms individually failed to grow by double digits in 2023. Of the 35 firms that failed to grow by 10% or more, 20 of them were ranked in the bottom 50.

For firms on the outside, looking in – this is where the opportunity for entry is relatively open. The barrier for entry into the Business Insurance’s Top 100 hasn’t risen significantly in the past ten years. A broker needed $23.6M to enter the top 100 in 2013. Today – they would need $31.3M (only a 33% growth in revenue since 2013). A significant task for many firms, but not impossible to imagine.

Six new additions to the top 100 list

As the consolidation of insurance brokerage firms continues, several firms from last year are no longer on the top 100 list – either because of acquisition or having not kept pace with the average YoY revenue growth rate of 13.5%. But with vacancy comes opportunity, and six firms have joined the top 100 list this year for the first time. These firms include:

- Crest Insurance Group enters the top 100 list at #70 with $59.1 million in revenue (a 11.1% YoY increase). Crest completed one publicly announced transaction in 2023, after completing two in 2022, and eight in 2021.

- Choice Financial Group enters the top 100 list at #85 with $45.4 million in revenue (a 23.5% YoY increase). Choice Financial Group completed six publicly announced transactions in 2023, after completing 10 in 2022.

- Hotchkiss Insurance enters the top 100 list at #93 with $40.2 million in revenue (a 17.3% YoY increase). Hotchkiss completed one publicly announced transaction in 2023.

- Brightline Insurance Group enters the top 100 list at #98 with $34.5 million in revenue (a 23.8% YoY increase). Brightline did not publicly announce any M&A transactions in 2023 or 2022.

- The Cason Group enters the top 100 list at #99 with $31.7 million in revenue (a 19.1% YoY increase). The Cason Group did not publicly announce any M&A transactions in 2023 or 2022.

- Engle-Hambright & Davies enters the top 100 list at #100 with $31.3 million in revenue (an 8.0% YoY increase). Engle-Hambright & Davies did not publicly announce any M&A transactions in 2023 or 2022.

How can firms grow and compete if they aspire to make or remain on the list?

Sustainable organic growth fueled by predictable sales velocity continues to be the most controllable method for taking an insurance brokerage firm to the next level – for increasing revenue and for attracting possible partners. Here are common strategies that firms of all shapes and sizes should address.

- Reassess your capital structure to build capacity and capital for growth.

- Re-think your risk tolerance as it relates to debt and leverage.

- Deliver a process driven new client acquisition strategy.

- Embrace aggressive new business goals and real production accountability.

- Build industry vertical specialization supported by data analytics.

- Double down on hiring new production talent.

- Design a wealth creation perpetuation plan to attract and retain talent.

Building a cultural commitment to an organic growth strategy, identifying potential best-in-class agency partnerships, and doubling down on opportunities for reinvestment (capital, talent) can be keys to the future outlook and success of firms that wish to compete to make the coveted Top 100 Broker List.